When agents do the work they absorb the context judgement is built from - leaving humans to decide more, and understand less.

Until recently, when a hailstorm broke your roof, the person who came to assess it was called an adjuster - not an assessor, not an inspector. The word is from a nineteenth-century trade in which the loss was never quite what the policy said and the policy never quite what the loss demanded, and the adjuster's job was to move one toward the other until both sides could sign. The work was a day of small actions: measuring, photographing, checking code, comparing claims. The judgement was a single minute inside it. We are now, without anyone announcing it, in a world where software can do the day and not the minute.

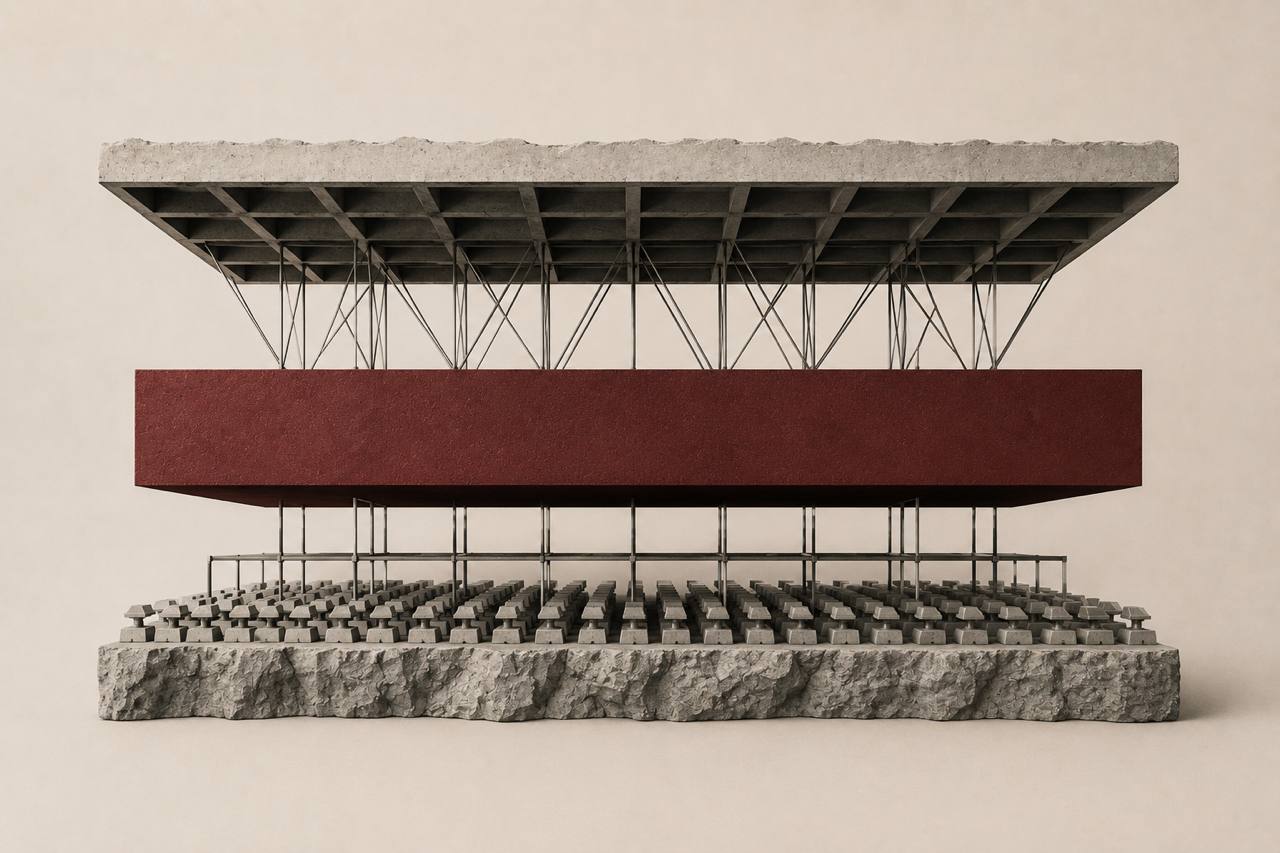

The indivisible unit, divided

Forty years of strategy rests on a unit everyone treated as solid. Michael Porter's insight in the 1980s was that a firm is not a black box but a chain of activities - discrete steps, each adding cost and value. The activity was the atom of strategy, and like the atom it was assumed indivisible. You could outsource one, automate parts, benchmark it against rivals. You could not take it apart. You can now.

An activity is three particles, and they are not equal. Two are inputs; the third is not.

Process - the doing: fill the form, run the reconciliation, inspect the roof. It can be automated.

Particulars - what make one firm's version differ from another's: the underwriting heuristic, the memory of every borrower who defaulted, what Oliver Williamson called asset specificity. They can be copied or learned.

Principal - the one who directs the process, brings the right particulars to bear, owns the outcome, and carries the liability. This is not an input at all.

"Who do I sue?" is not a footnote to enterprise; it is the question that gives American capitalism its shape, as "who answers to the regulator?" gives Europe's. The principal is the only particle that answers, and answering is something a person or a firm must consent to do.

These three lived in one body because they had to: the only place a firm's experience lived was in the head of someone it could fire. They held like a chemical compound - not by design, but because nothing could break the bond. An AI agent breaks it. Stripped of the marketing, an agent is a machine that reads across systems, infers what is happening, acts, and logs what it did. It does not replace the adjuster's minute. It replaces the seven hours around it.

In the technical stack the mapping is exact for two of the three. The model runs the process. The harness around it - memory, retrieval, the firm's data and configuration - holds the particulars. The third has no home in the stack at all: there is no component that is the principal, because the one thing you cannot encode is the consent to be sued for what comes out of the other two.

And this is where the particulars turn dangerous to their owner. As the model commoditises - prices collapsing, benchmark leads gone within months - value has migrated to the harness: the scaffolding of memory, context and relationships that, over time, is the firm's accumulated specificity made legible. The firm that runs its activity on a third party's platform is pouring those particulars into a layer the platform has every incentive to learn from. It believes it is renting a process; in truth it is feeding its specificity into a system built to absorb it. The naïve adopter gives away the two particles it might at least have defended - and is left holding the one it cannot give away: the liability. That is the quiet trade of the agentic economy, and many firms are making it without noticing.

Accountability does not follow the work

The obvious inference - that whoever does the work answers for it - is wrong, and Klarna proved it in public. Its AI assistant did the work of 700 customer-service agents, by the company's own count; fourteen months later the chief executive was walking it back, conceding "lower quality" and rehiring humans. Read as "AI can't do customer service," this misses the point. The agent did most of the work well. Two things failed together: the work degraded on the hard tail - the distressed dispute, the non-standard claim, where judgement is threaded through the doing rather than waiting at the end - and the firm had pulled the work out of the activity with nowhere for accountability to live. No escalation logic, no authority limits, no line between what the agent settled and what a human owned. Remove the work and the supervision does not look after itself.

The pattern repeats wherever oversight used to be a by-product of execution. A radiologist's software now reads the scan, but the consultant's signature is no longer a reflex of having read it - it is a separate, deliberate act. A content model removes the post; a human reviews the removal on a delay. The work moves to the machine; the accountability stays, but has to be rebuilt - into evaluation suites scored against business outcomes, authority limits, audit trails a regulator can reconstruct, recovery procedures for when the agent is confidently wrong. None of this is the agent's work. All of it is the firm's, and almost none of it existed before.

So the strategic question is no longer what activities do we perform? It is, for each activity, which particle carries the weight, and what happens when the bundle comes apart?

Why the firm survives

That the firm is restructuring into layers is, by now, consensus - the governance layer, the dissolving moat, the "headless firm" coordinated by protocol. What the consensus underplays is that the new layer does not look like an AI project. It looks like compliance or risk with the label filed off - and a risk function that assumes it already does this will find it is sized for human error rates, not for an agent that fails fast, at scale, and with complete confidence. Klarna thought it had bought an agent. It had bought one particle of an activity, with the other two unbuilt.

Push the logic far enough and the firm itself seems to dissolve: if the work runs on software, supervision can sit anywhere, and the particulars are just data, then Coase's 1937 account of why firms exist begins to fail. The maximalist version - argued loudly now - has the surviving company at a tenth of today's headcount, enduring only as a "fiduciary wedge," a legal shell holding liability, IP and capital while the work disperses to agents. Economists at MIT, Harvard and Boston University take the force seriously: as agents absorb the tasks that make up transaction costs, the make-or-buy line that defines the firm will move. Tellingly, they expect human effort to shift toward judgement, oversight and relationships - the three particles seen from the economists' side of the room.

But the firm does not dissolve - it contracts to what cannot leave. The principal can be shifted - into a captive insurer, an indemnity clause, a special-purpose shell - but never shed: the liability snaps back inside the instant something breaks, the oldest pattern in commerce and the one software is least able to touch. The maximalists are right that the work leaves and wrong about what remains. What they dismiss as a fiduciary shell is the new corporate competence, and where the next decade's strategic action lives.

The principal's price

This is about to become the central commercial fight of the agentic economy. Vendors want to price for the human work they replace - to charge as if they had absorbed the underwriter, the analyst, the paralegal - while their contracts do the reverse, capping liability at fees paid and increasingly requiring the customer to indemnify the vendor for the model's own output. They want the principal's price without the principal's exposure. But the principal is the one particle that cannot be sold; a buyer paying substitution rates while keeping all the liability has paid for a transfer that never happened. The collision is already visible where the stakes turn physical: as software contracts push liability onto the buyer, safety law pushes it the other way - Britain's Automated Vehicles Act puts the blame for a self-driving crash on the manufacturer, not the passenger. The frontier-model business model is steering toward rocks the car industry has already hit.

The cost no one is pricing

There is a cost that appears in no productivity figure. The seven hours were not only cost - they were where judgement was formed. The adjuster who spent the day on the roof reached the minute already knowing it; the context accrued in the doing. Strip the doing away and the minute does not stand alone, rested and whole. It becomes one of hundreds, made cold. Engineers working with coding agents describe it exactly: the job shifts from writing to evaluating, and judging another's code takes at least the competence of writing it - more, because the reasons behind it are missing. The day becomes back-to-back decisions with no runway between them: faster, and far more draining. Researchers call the durable form "cognitive debt," and its failure mode is quiet - it surfaces in the crisis, when something breaks and the people nominally in charge no longer hold the context to fix it. A firm that decomposes its activities without seeing this has not removed the judgement. It has concentrated it, stripped its context, and handed it to people it is quietly burning out.

The adjuster still has a job. Software scans the roof, measures the damage, pulls the comparables, and the day compresses to an hour. But the minute - this roof, this policy, this customer, what is fair - is still a minute, and someone must still answer for it. Everything around it has changed. The work is lifted off. The particulars are being copied and learned. What remains, exposed, is the principal: the one who owns the outcome and is still there to be sued when the agent is confidently wrong. The specificity that set one insurer apart is revealed as the asset it always was - and the willingness to answer for it as the scarcer thing still.

If your firm is navigating the agentic transition, book a call with Lion Strategy. We help boards and investors understand where value lives when the work leaves.

For corporate leaders

Name an owner. The capability sits between the people who build agents and the people who govern them, and reports cleanly to neither. Unowned, it does not get built. This is a board appointment, not a delegation.

Keep it away from risk-as-usual. Compliance is calibrated for human error. Agents fail faster, at scale, with total confidence. Evaluation suites, authority limits, audit trails and recovery procedures are new infrastructure, not an extension of the old.

Protect the context, not just the headcount. The people left holding the judgement now make back-to-back calls without the context the old work supplied. Build it back deliberately - review-load limits, rotation, time to understand the system rather than only sign off on it - or judgement fails exactly when you need it.

Start with one activity. Take the one where work most outweighs judgement, run it through an agent, and build the supervision around it. The architecture is learned by doing it once, not planning it for everyone.

For investors

Re-underwrite the moat at entry. Separate the encoded work, dissolving into a shared substrate, from the specificity and relationships that harden as the work commoditises. You are often paying a workflow premium for an asset whose value is the data and the relationships.

Scrutinise mid-market software first. Everyone says these moats are dissolving; the question is which half - the workflow, which commoditises, or the data and customers beneath it, which don't. Not a signal to sell, but to know which you own before the market reprices it.

Treat supervision as the value-creation thesis in the hold. The portfolio company that builds it runs agents at a cost and reliability rivals cannot match - and as operating differences compress across a sector, that is what defends the multiple.

Notes

[1] Porter, Michael E., Competitive Advantage (Free Press, 1985).

[2] Williamson, Oliver E., The Economic Institutions of Capitalism (Free Press, 1985).

[3] Coase, Ronald H., "The Nature of the Firm," Economica 4 (1937).

[4] Shahidi, Rusak, Manning, Fradkin and Horton, "The Coasean Singularity?" in The Economics of Transformative AI (NBER, 2025).

[5] Klein and Wieczorek, "The Headless Firm" (arXiv, 2026); and the maximalist case, Ismail and Diamandis, "The Organizational Singularity," Moonshots EP258 (2026).

[6] Klarna - company announcement (Feb 2024) and Sebastian Siemiatkowski's remarks on service quality (May 2025), as reported by Bloomberg and others.

[7] Enterprise AI terms typically cap liability at fees paid and invert indemnification onto the customer; see surveys of frontier-model terms of use (2026). Self-driving liability - UK Automated Vehicles Act 2024, placing responsibility on the manufacturer / authorised self-driving entity.

[8] Bessemer Venture Partners, "AI Infrastructure Roadmap: Five Frontiers for 2026" ("as models become commoditised, differentiation shifts to the memory and context layer"); and Insight Partners, "2026 Investor Predictions" (durable advantage shifting to customer intelligence and domain expertise as model labs push into the application layer). Frontier-model prices fell steeply across providers through 2025-26.

[9] Kosmyna et al., "Your Brain on ChatGPT" (arXiv, 2025), a preliminary MIT Media Lab study; and practitioner accounts of the shift from writing to evaluating in software engineering.

Elliot Ronald is the Founding Partner of Lion Strategy, a strategy consultancy working with boards and executives on AI sovereignty and the agentic age.